Money feels simple until a founder has to raise it under pressure. Startup funding rounds are staged investments that help a young company move from a risky idea to a larger business with customers, staff, systems, and investor expectations. Seed funding usually pays for proof. Series A funding pays for a repeatable model. Series B pushes growth harder. Series C often supports expansion, acquisitions, or a path toward sale or public markets. That sounds neat on paper, but real fundraising in the USA is messier. A founder in Austin may raise from angels first. A SaaS team in Boston may skip a priced seed and use a SAFE. A consumer brand in Los Angeles may avoid venture capital investors for years because margins need patience. The point is not to chase a round name. The point is to know what each stage demands before you give away equity, change your board, or promise a growth curve you cannot defend. Strong fundraising also depends on trust, public proof, and founder credibility signals that make outsiders believe the company has a real market behind it.

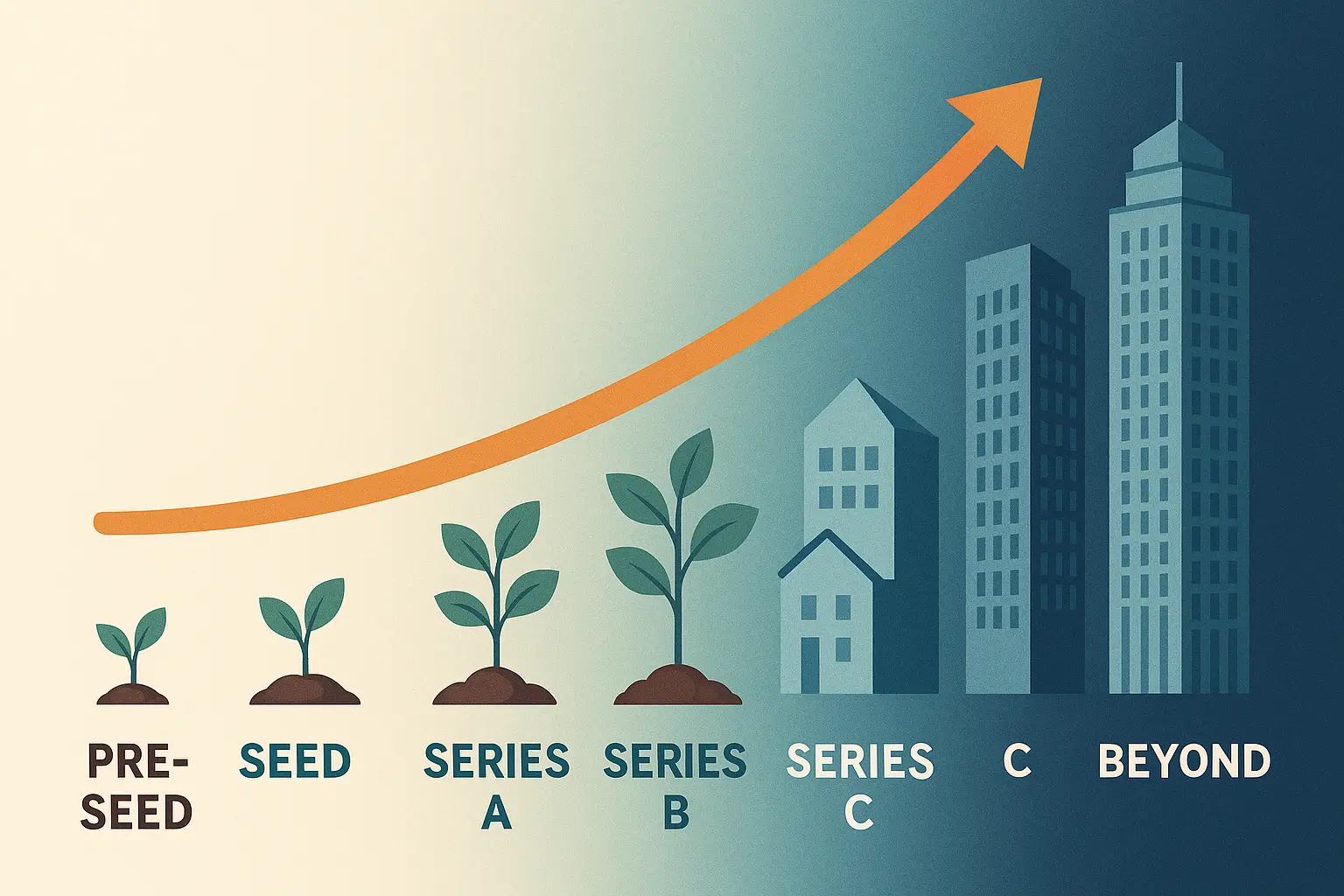

How Startup Funding Rounds Change as the Business Proves Itself

Every raise answers one hard question: what has changed since the last risk was taken? At the beginning, the risk is whether anyone cares. Later, the risk shifts toward sales motion, hiring, unit economics, and market size. That is why the same pitch cannot work from seed to Series C. The company may keep the same name, logo, and mission, but the proof needed at each stage becomes heavier. A founder who ignores that shift ends up pitching yesterday’s company to tomorrow’s investor. That is when meetings feel polite, slow, and doomed.

Why Seed Funding Is About Evidence, Not Perfection

Seed funding is often misunderstood because founders treat it like a small version of a later round. It is not. A seed investor is usually buying into evidence that something unusual is starting to form. That evidence might be a small group of paying customers, a waitlist with real intent, a technical prototype, or a founder who has lived the problem for years. The work is less about looking finished and more about showing that the founder can keep reducing uncertainty.

A Chicago logistics startup, for example, might not need national revenue at seed. It may need five regional trucking firms using the tool each week and telling the founder they would be angry if it disappeared. That kind of proof is not polished, but it is alive. Investors can work with alive.

The non-obvious part is that too much polish can hurt a seed pitch. A 40-slide deck full of smooth forecasts may make the company feel staged. At seed, a sharp investor often wants to see the messy learning trail: who said no, what changed after the first ten demos, why the current product is narrower than the first idea. That trail proves the founder can listen without drifting.

What Investors Expect Before Series A Funding

Series A funding usually comes when a company can show the first signs of repeatability. This is where many founders get surprised. A few big customers may not be enough, because investors want to know whether the company can keep finding the same kind of buyer without the founder hand-carrying every sale. In a tight U.S. funding market, repeatability often beats charm.

For a B2B software company, that may mean a clear customer profile, a sales cycle that can be explained, retention that is not held together by favors, and pricing that has survived real pushback. For a direct-to-consumer brand, it may mean a customer acquisition channel that still works after early friends and fans are exhausted. This is also where early-stage business planning starts to matter in a less romantic way, because venture capital investors will study how money becomes motion.

The trap is raising Series A money to discover the model. That can happen, but it is expensive. Once a priced round sets a valuation, the company has made a public bet inside a private market. Miss that bet, and the next raise may become a bridge, a flat round, or a hard conversation about whether the company grew ahead of its own proof.

The Real Meaning of Seed, Series A, Series B, and Series C

The names sound like school grades, but the work behind them is closer to a loan application, a hiring plan, and a court case combined. You have to show why the business deserves capital, how it will spend that capital, and why the result should be worth more later. The U.S. Small Business Administration describes venture capital as investor funding that is commonly exchanged for ownership, which is a useful reminder: this money is not free cash. At every stage, the founder is selling part of tomorrow’s upside to buy time, talent, and proof today. It changes who shares the upside and who gets a voice in the company. That voice may be helpful, but it is still a voice at the table when budgets, hires, exits, and future raises are discussed. U.S. Small Business Administration’s funding guide

How Seed and Series A Build the Base

Seed and Series A sit close together, but they reward different behavior. Seed rewards learning speed. Series A rewards pattern recognition. A founder raising seed can say, “We found a painful problem and built the first answer.” A founder raising Series A needs to say, “We know who buys, why they buy, how much they pay, and what it takes to reach more of them.”

Think about a Miami health-tech startup selling scheduling software to small clinics. At seed, ten clinics using the product may be enough to prove the pain. By Series A, the investor will ask whether clinics in Phoenix, Nashville, and Denver behave the same way. Local luck has to become repeatable demand, and that shift can expose weak onboarding, unclear pricing, or a founder-led sales process that no hire can copy.

The strange thing is that Series A can feel less creative than seed. Seed may reward wild insight. Series A rewards discipline. The founder who keeps adding features may lose to the founder who cuts half the roadmap and wins one narrow customer group with care. The best Series A pitch often has fewer claims than the seed pitch, not more; it replaces excitement with proof.

Why Series B and Series C Raise the Stakes

Series B is where the company has to grow without cracking. The product may work. The sales motion may work. Now the question is whether the company can add people, territories, channels, and leadership layers without slowing down or damaging the customer experience. Many founders discover here that culture, finance, and process are not side issues; they are what keep growth from turning sloppy.

A Series B e-commerce software firm in New York might use funds to build enterprise sales, improve security reviews, and open a second office. Those moves sound grown-up. They also add drag. More staff means more meetings, bigger customers mean longer contracts, and higher revenue can hide weak margins if nobody is watching the cost of support.

Series C often points toward a larger map. The company may enter new markets, buy a smaller competitor, build a second product line, or prepare for an acquisition conversation. Some companies use Series C to strengthen the balance sheet before a wider market push, while others use it because the earlier growth plan worked and the next move needs more capital than revenue can supply. The counterintuitive lesson is that later money can be more restrictive than earlier money, because the check is larger but the room to wander is smaller.

What Each Round Costs Founders Beyond Equity

Founders talk about dilution because it is easy to count. Ownership drops from one percentage to another, and the math looks clean. The deeper cost is control of pace. Each raise adds a clock. Once outside money enters, the company is no longer judged only by survival. It is judged by progress against the story that won the money. Employees feel that clock too, even when nobody says it out loud. Hiring plans, product deadlines, and sales targets start to carry investor weight.

How Dilution, Valuation, and Control Connect

Dilution is not automatically bad. Owning a smaller piece of a stronger company can beat owning all of a stalled one. The problem starts when founders treat valuation as a trophy instead of a tool. A high valuation can feel like victory on announcement day, then become a trap if the company cannot grow into it.

Say a San Francisco AI startup raises a large Series A at a rich valuation during a hot market. The team hires fast, signs a large lease, and builds for a demand curve that looked certain. A year later, buyers slow down. The next investors may still like the company, but they may not like the old price, which is how a proud raise can lead to a painful reset.

Venture capital investors also care about terms, not only valuation. Liquidation preferences, board seats, pro rata rights, option pool changes, and protective provisions can shape the founder’s room to move. The headline number rarely tells that story. A practical founder reads the term sheet like a future argument: what happens if the company sells early, who approves a new round, and how much option pool expansion comes out of the pre-money valuation? The best time to understand control is before anyone is tired, rushed, or afraid of losing the deal.

Why Capital Can Distort Good Judgment

Money gives a company room to breathe. It can also make poor habits look smart. A bootstrapped team may notice waste because waste hurts that week. A funded team can hide waste inside growth plans, brand campaigns, and hiring waves that sound impressive during board updates. The bank balance can become a fog machine. Teams may keep projects alive because they can, not because customers asked for them. That is how funded companies drift while looking active.

One odd risk is that funding can pull a founder away from customers. Before seed funding, the founder may spend each day in demos, support chats, and sales calls. After a round, the calendar fills with recruiting, investor updates, finance reviews, and leadership meetings. Those tasks matter, but the market does not care how busy the founder feels.

This is why a startup financial planning checklist should include behavior, not only budget lines. Who talks to lost customers every month? Who reviews churn notes? Which spend gets cut first if sales lag? The best founders treat each raise as rented confidence: the money gives them a chance to prove the next claim, but it does not prove the claim by itself.

How to Choose the Right Funding Path for a U.S. Startup

Not every company should raise through the classic venture path. That sentence bothers some founders because fundraising has become a status signal. Yet a company can be strong, profitable, and valuable without ever taking Series B or Series C money. Recent private-market reporting from Carta showed more capital flowing again in 2025, but that does not mean every founder should chase the same path. More available money can tempt the wrong company into the wrong deal. The smartest move is to separate market mood from company need. Capital should answer a business question, not a social one. A raise should make the next milestone more believable, not make the founder feel more accepted.

When Venture Capital Investors Make Sense

Venture capital investors make sense when the market rewards speed and the company can grow large enough to return the fund’s bet. A cybersecurity platform, biotech tool, fintech network, or infrastructure software company may need capital before revenue can carry the full load. In those cases, waiting too long may let a better-funded rival win distribution. Speed has a price, but slow motion has one too. In markets with winner-take-most dynamics, being careful for too long can hand the category to someone else.

A Denver founder building software for local home service companies may not need venture money if the market grows through steady sales and strong cash flow. A founder building a payments network across thousands of U.S. merchants may need outside capital because networks take time, trust, and early spending before they become defensible. The subtle point is that venture money is less about being a “better” business and more about being a certain kind of business.

Investors need outcomes large enough to cover losses across a portfolio. A healthy company that could sell for $25 million may be life-changing for a founder, but too small for many funds. That mismatch creates bad advice. A venture investor may push a company toward bigger risk because the fund needs a larger result, while the founder may prefer a durable business with less drama. Neither side is wrong. The goals differ.

When Alternative Capital Is the Smarter Move

Many U.S. companies should compare venture with other options before signing away ownership. Revenue-based financing, SBA-backed loans, customer prepayments, grants, strategic partnerships, angel checks, and plain profit can all fund growth in the right setting. The tradeoffs vary, but they may fit a business that does not need to chase a billion-dollar exit.

A bootstrapped education company in Raleigh might grow through school district contracts and annual renewals. Venture money could force it to expand before procurement cycles are ready. A small manufacturer in Ohio might do better with equipment financing and customer deposits than with a fund that expects software-like margins. This is not anti-venture. It is pro-fit. The quiet win may be a company that pays the founder well, serves a clear market, and never needs permission from a board to stay sane.

A founder should ask whether the company’s natural growth curve matches the pressure of institutional capital. If the answer is no, the cleaner path may be slower on LinkedIn and stronger in real life. A useful test is simple: would the company still want the plan if no funding announcement came with it? If yes, capital may be fuel. If no, capital may be ego wearing a blazer.

Conclusion

The path from seed to Series C is not a ladder every founder must climb. It is a set of tradeoffs that should match the company’s proof, market, and appetite for pressure. Seed asks whether the problem is alive. Series A asks whether the model repeats. Series B asks whether growth can survive weight. Series C asks whether the company can play on a larger field without losing its center. The best founders understand startup funding rounds as commitments, not trophies. They raise when the next risk is clear, the use of funds is sharp, and the business can defend the story it tells. That discipline matters more in the USA now because capital is still available, but patience is thinner than it was during the easy-money years. Before you chase the next stage, write down what the money must prove, what control you may lose, who gains influence, and what happens if the plan takes twice as long. Raise for the company you are building, not the headline you want people to share.

Frequently Asked Questions

How much equity do founders usually give up during seed funding?

Many seed deals land somewhere between a modest ownership sale and a larger early dilution, depending on valuation, traction, and investor demand. The better question is whether the money buys enough runway to reach the next proof point without forcing a rushed raise.

Is Series A funding possible without strong revenue?

Yes, but it is harder. Investors may still back a company with deep product usage, strong retention signals, or a market that is opening fast. Revenue gives cleaner proof, though, especially when buyers are paying without special discounts or founder favors.

What is the main difference between angel investors and venture firms?

Angel investors usually invest personal money and may move faster with lighter process. Venture firms invest from a fund, answer to their own investors, and often need larger outcomes. Angels may fit earlier tests, while firms often expect a bigger growth path.

Should a startup raise Series B if it is already profitable?

Profit does not rule out Series B. The real question is whether outside money can create a larger result than profits alone. If the company can grow at the right speed without selling more ownership, staying independent may be the wiser move.

How long should each funding stage last?

Many founders plan for 18 to 24 months of runway, but market conditions, burn rate, and sales cycles can change that. A company with long enterprise deals may need more cushion than a consumer app that can test growth channels each week.

What do investors look for before Series C?

They usually want proof that the company can expand with less guesswork. That may include strong revenue quality, leadership depth, clean reporting, market power, and a believable exit path. At this stage, weak operations can damage even an exciting growth story.

Can a startup skip from seed to Series B?

It can happen, but it is uncommon and depends on rapid traction. A company would need proof strong enough to answer many Series A concerns at once. More often, founders use a larger seed extension or a priced Series A before attempting Series B.

Is venture capital the best option for every startup?

No. Venture works best when the market is large, growth can be fast, and the founder accepts pressure for a major exit. Service firms, local companies, steady software tools, and niche brands may do better with loans, profits, customers, or strategic partners.